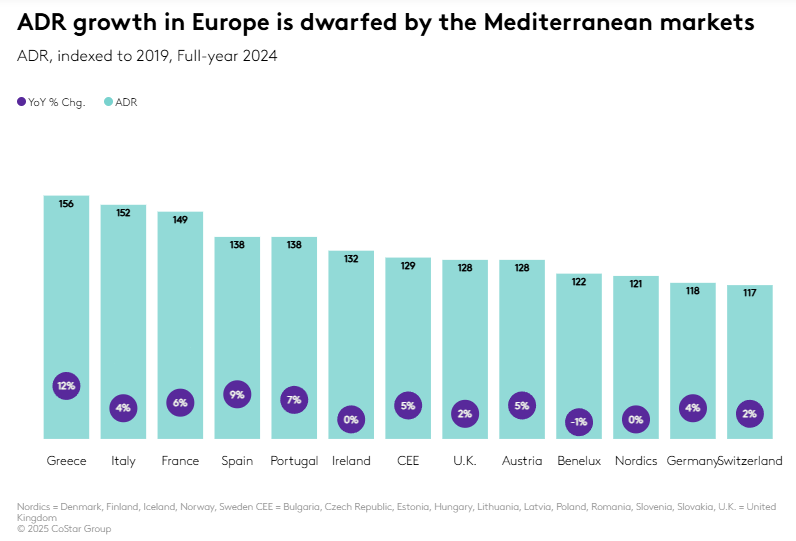

The Southern European hospitality market experienced another year of high performance in 2024, with the region’s revenue per available room (RevPAR) index growing by 9.8% year-on-year, as the allure of its beaches and historic cities attracted leisure travellers from around the world. This strong demand led to an 8% rise in the average daily rate (ADR), which stood at €175 – the highest regional rate in Europe for the year, with Greece being the market with the highest increase in the index (12%), compared to pre-pandemic 2019, according to CoStar‘s latest data.

The 2024 Olympic Games in Paris have provided the French hospitality market with a significant increase in demand. Paris, of course, experienced the strongest impact, with hotels maintaining an 80%+ occupancy rate during the two weeks of the Games and reaching 90.5% midway through the period.

However, the real winner was ADR, which averaged EUR 781 during the event. All Parisian submarkets benefited from increased demand, although RevPAR was strongest in areas close to the Olympic venues and key tourist attractions: Champs Elysees, Louvre/Marais and Opera/Grasse Boulevard. However, the Games did not only benefit Paris. RevPAR of French hotels outside Paris increased by 12.4% in July and 17.2% in August, as the Olympics highlighted French destinations and culture beyond the capital.

Spain also witnessed another remarkable year of double-digit growth, as the rise in international tourism contributed to an 11.5% increase in RevPAR compared to 2023. Major cities such as Madrid and Barcelona, known for their cultural richness and vibrant nightlife, led the country with RevPAR growth of 14.0% (Madrid) and 7.7% (Barcelona).

Coastal destinations such as the Balearics and the Canary Islands also recorded a more controversial tourism boom. In the Balearic Islands, 2024 ended with an occupancy rate of 68.4%, just above the pre-pandemic level, and a 10.7% increase in RevPAR compared to 2023. While occupancy in the Canary Islands didn’t quite exceed the 2019 level, rates impressed more than that, growing 10.2% year-over-year and exceeding pre-pandemic levels by more than 37%.

Spain is not the only Southern European market struggling to absorb such a significant influx of tourism. Overtourism has emerged as a critical threat across the region, affecting popular destinations and local communities. The strain on local resources has led to a variety of responses in 2024, from resident-led protests in Spain to more formal government involvement, such as tourism taxes and visitor caps in Italy.

Despite both unorthodox and more official approaches to dealing with over-tourism, both occupancy and ADR in Athens, Rome, Venice and the Spanish islands continued to increase in 2024. The forward-looking figures further suggest that measures to address over-tourism have not yet deterred most travellers, as occupancy on the books continues to increase on an annual basis for many Southern European markets even in the most subdued off-season period.

Paris is looking forward to a year of consolidation after the Olympics (2024) and the Rugby World Cup (2023). Italian markets will seek to continue to attract long-haul travellers through more direct flights to the US and the Asia-Pacific regions. For Spanish markets, balancing local needs and traveler demand will be a top priority.

{kind=link}