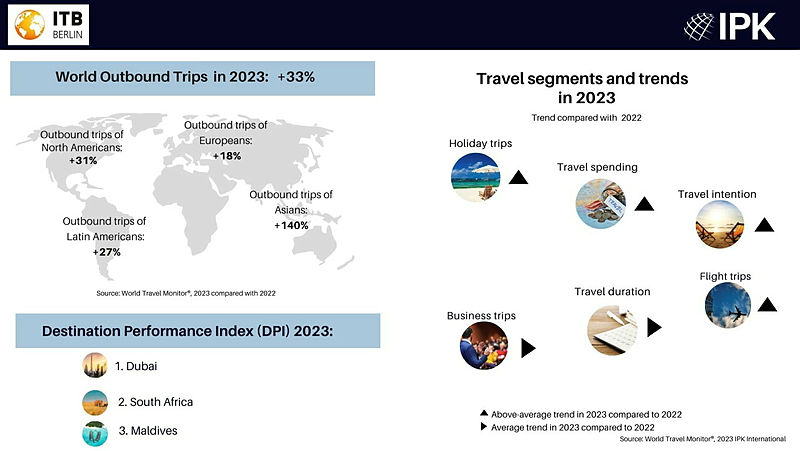

Outbound travel recorded a double-digit increase of 33% in 2023, compared to 2022, down 12% from pre-pandemic 2019, marking another big step towards a return to pre-pandemic levels, with a full recovery projected in 2024, according to the findings of IPK International’s latest World Travel Monitor on global outbound travel trends, presented by ITB Berlin.

Positive signs are mainly the gradual return of outbound travellers to Asia and the upward trend in holiday travel.

Despite rising travel costs, interest in outbound travel remains high this year, and what is notable is that travel satisfaction is emerging as an increasingly important factor.

According to IPK’s World Travel Monitor®, the return of outbound travel to Asia with annual growth of over 140% is the main growth driver in 2023. Although still 37% below 2019 levels, this marks a significant upward trend.

Compared to 2022, outbound travel to Europe increased by 18%, North America by 31% and Latin America by 27%.

In 2023, outbound travel volume was highest in the US, with Germany next and the UK third. Taken together, these three tourism ‘source’ markets accounted for a third of global outbound travel volume last year.

Spain as a reference point

With a share of almost 10%, Spain was again the most visited destination worldwide in 2023, followed by the USA.

IPK’s Destination Performance Index (DPI) found that Dubai was the highest scoring destination in 2023. To establish the DPI, World Travel Monitor® took into account all global outbound holiday travel in terms of travel satisfaction, whether travellers would recommend a destination to other travellers and their desire to return to that destination in the future.

Among the top five highest scoring destinations behind Dubai was the Maldives, last year’s winner, followed by South Africa and Abu Dhabi.

Austria and Switzerland were the highest-scoring destinations in Europe.

Increased demand for sun and beach holidays

Compared to 2022, holidays as a reason to take a trip have once again improved their market share. In 2023, three quarters of global outbound trips were for holidays. Within this segment, sun and beach holidays and city breaks dominated, each taking up around a third of the market. Return trips were in third place.

What is surprising is that the market shares of these three travel categories have moved in different directions over the last three years, but are now at similar levels to 2019.

This suggests that the pandemic has not materially changed people’s holiday choices. In 2023, the main factors for a holiday trip abroad were relaxation, sightseeing, fine dining and shopping.

Air travel gets the biggest part

In 2023, over 60% of outbound trips were made by air, making air travel the most popular form of transport for international travel. However, it’s worth noting that when travellers were asked how they get to their destination of choice, the majority cited public transport. While, a fifth said they used a rental car.

Significant increase in travel expenses in 2023

Due to the increased cost of travel, especially air travel, travel expenses increased above average in 2023, while the average number of nights remained stable at around nine.

On the best and worst aspects of a trip, travellers chose ‘value for money’, both from a positive and negative perspective. Other factors that are important to travellers are accommodation, food and the natural environment of the area.

Full “come back” by the end of 2024

Some travel destinations and travel markets have already recovered to 2019 levels, while others are lagging behind. In 2023, some destinations were again affected by over-tourism effects. A third of respondents said they felt their destination was characterised by overcrowding. Nevertheless, the latest findings from the World Travel Monitor® predicting global outbound travel trends for the next 12 months are positive and set the stage for a full recovery in almost every market and segment by the end of 2024.

{kind=link}