Europe’s hotel industry reported mostly positive results in the three key performance metrics during Q1 2019, according to data from STR.

Euro constant currency, Q1 2019 vs. Q1 2018

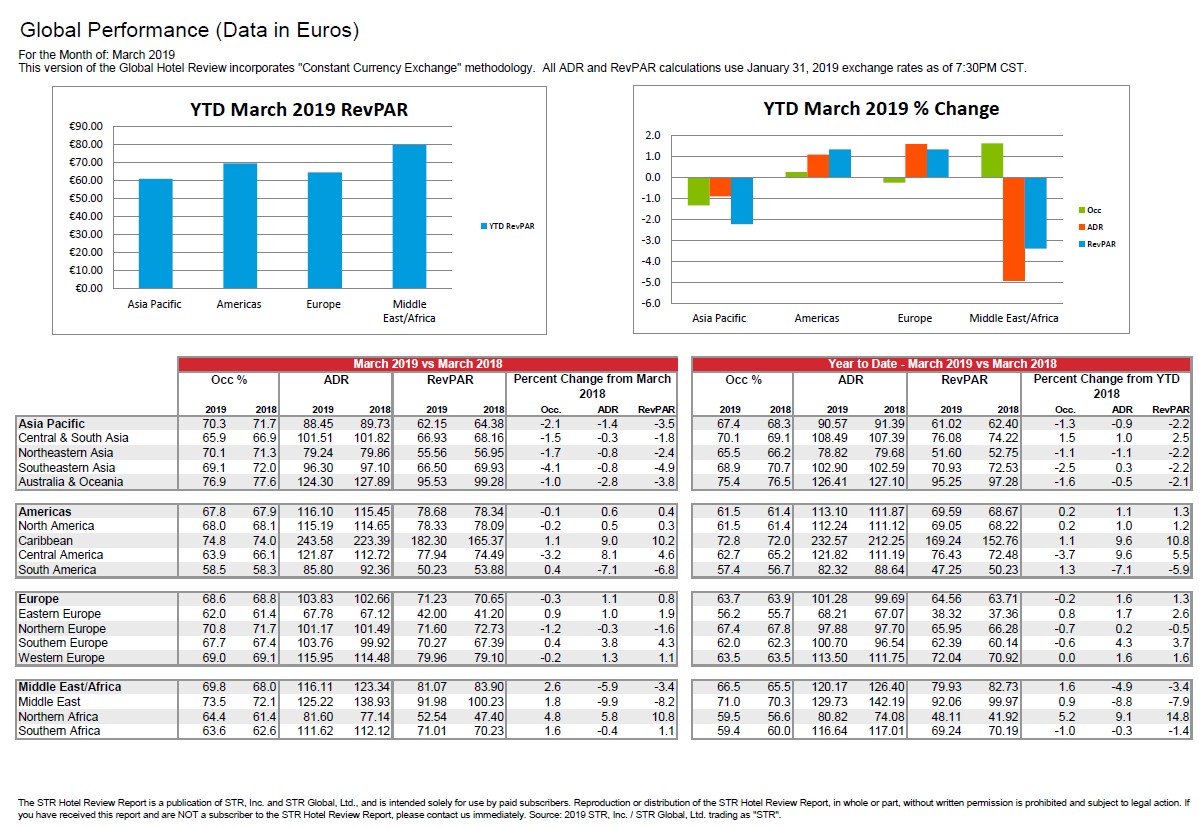

Europe

- Occupancy: -0.2% to 63.7%

- Average daily rate (ADR): +1.6% to EUR101.28

- Revenue per available room (RevPAR): +1.3% to EUR64.56

Local currency, Q1 2019 vs. Q1 2018

Madrid, Spain

- Occupancy: +2.6% to 71.1%

- ADR: +5.7% to EUR106.79

- RevPAR: +8.4% to EUR75.95

The absolute occupancy and RevPAR levels were the highest among first quarters with the most complete samples in STR’s Madrid database. STR analysts attribute a 4.4% rise in demand (room nights sold) to major events hosted in the market, such as Mercedes Benz Fashion Week Madrid (24-29 January), ARCOmadrid (27 February-3 March), World ATM Congress (12-13 March), Motortec Automechnika (13-16 March) and the annual match between Real Madrid and Barcelona (2 March).

Athens, Greece

- Occupancy: -11.0% to 54.5%

- ADR: +1.9% to EUR103.34

- RevPAR: -9.3% to EUR56.32

STR analysts note that a 9.2% decline in demand in the market came in comparison with a strong Q1 in 2018, when the number of rooms sold grew 5.4% and RevPAR jumped 13.2%. At the same time, however, Athens’ absolute occupancy level was its worst for a Q1 since 2014.

New inventory played a role in the equation as a 2.0% increase in supply was the largest for a Q1 in the market for quite some time. Additionally, a surge in short-term rentals as outlined by AirDNA, is likely part of the explanation for how airport arrivals are up, yet hotel demand is down.