Negative performance (also) in July 2025 – for hotels in Athens.

The 7-month period of 2025 is at roughly the same levels as the 7-month period of 2024.

Measures and targets to ensure tourism “stability” are expected in view of the Thessaloniki International Fair.

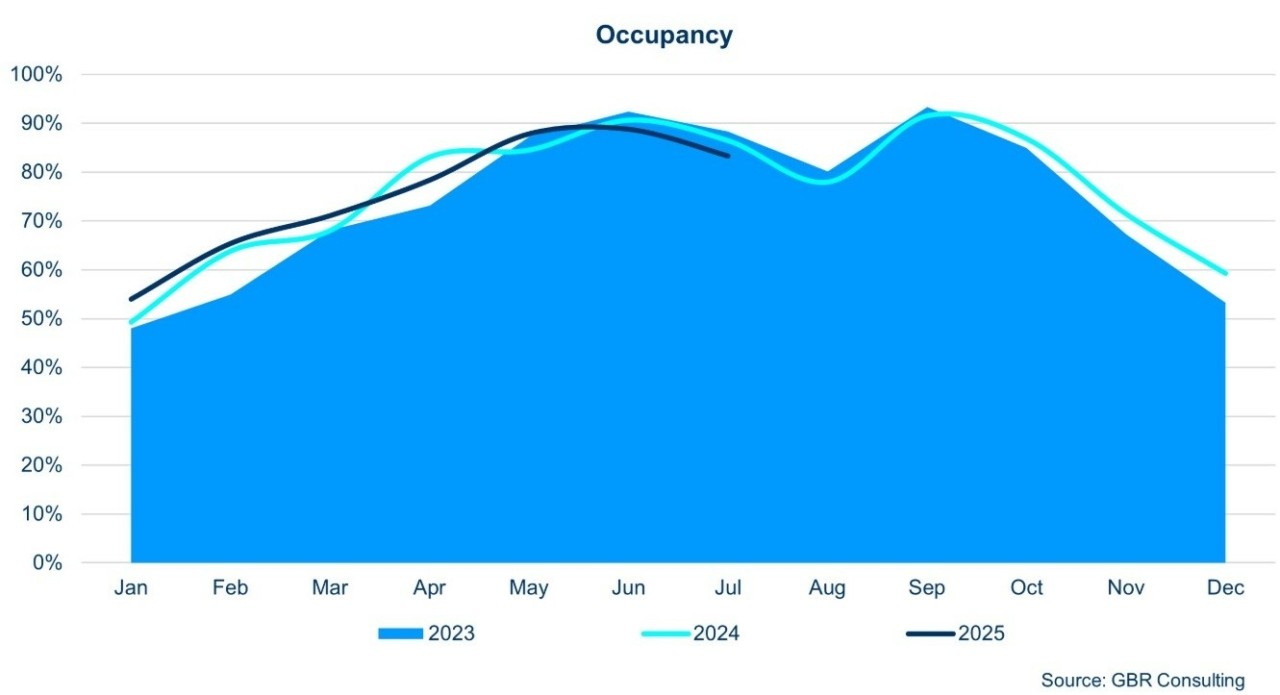

July ended with a decline for hotels in Athens – Attica, as the average occupancy rate stood at 83.3%, lower than the 86.4% recorded in the same month of 2024, according to data from the Athens, Attica, and Argosaronic Hotel Association.

Compared to July 2023, the decline is even greater, reaching 5.7%.

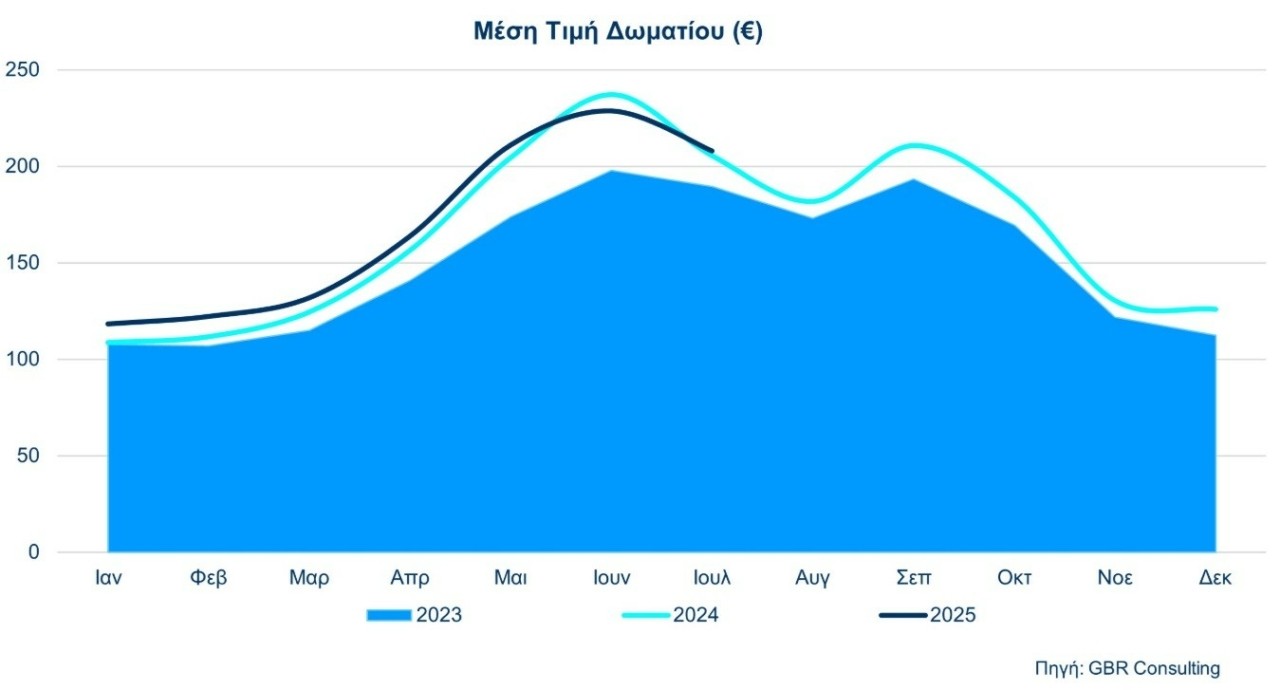

Although the average room rate (ADR) rose slightly to €207.85 (+1.1%), revenue per available room (RevPar) fell by 2.5% to €173.19.

However, the overall picture for the year so far remains positive. Between January and July 2025, occupancy rose marginally to 75.8%, the average room rate reached €176.18 (+1.6%), while RevPar rose by 2% to €133.49.

More specifically, the performance in July 2025 was not what Athens hotels would have liked to see—and, in a way, unfortunately, the prevailing atmosphere in terms of performance in June this year had prepared us for this. Although the first seven months of 2025 closed at roughly the same levels as the corresponding seven months of 2024, it is worrying that in July, at the height of summer, there was a decline in average occupancy and revenue per available room (Rev Par) in hotels, while the average room rate (ADR) remained at roughly the same levels.

More specifically:

July 2025 recorded an average occupancy rate of 83.3%, compared to 86.4% in July last year, representing a decrease of (-) 3.6%, following a June that also saw a 2% drop in average occupancy. It is worth noting that the corresponding negative change in average occupancy in July 2025 compared to July 2023 reaches (-) 5.7%. The Average Daily Rate (ADR) in July stood at €207.85, compared to €205.54 in July last year, i.e. a slight increase of 1.1%, while RevPar in July 2025 stood at €173.19, compared to €177.64 in July last year, representing a decrease of (-) 2.5%.

The traffic and performance of Athens hotels over the seven-month period closed at roughly the same levels as the corresponding period last year, which is mainly attributed to the better performance of hotels in the first quarter of the year: The average occupancy rate in Athens hotels during the seven-month period 2025 (75.8%) increased by 0.4%, the average room rate (ADR) stood at €176.18, an increase of 1.6% compared to the same period last year, while the average revenue per available room (Rev Par) reached €133.49 (an increase of 2% compared to the same seven-month period last year). Three-star hotels appear to be under particular pressure, with occupancy rates on a downward trend since March.

Compared to Athens’ competitor cities, Athens’ performance in terms of occupancy, average room rate, and revenue per available room continue to be better than those of Istanbul, but lag behind those of Barcelona, Madrid, and Rome. In particular, in terms of average room rate (ADR), there was an increase of 1.6% for Athens, 3% for Rome, 4.9% for Madrid, and 2.4% for Barcelona, while Istanbul saw a decrease of (-)1.9%. Similarly, in terms of revenue per available room (RevPar) during the seven-month period, there was a decrease of 2% for Athens, while Madrid saw an increase of 4.8%, Barcelona an increase of 1.3%, Rome an increase of 2%, and Istanbul recorded a decrease of (-)3% compared to the same period last year.

In terms of competition, Athens continues to outperform Istanbul, but lags behind other major European destinations. In particular, the increase in the average room rate in the Greek capital lags behind Rome (+3%), Madrid (+4.9%), and Barcelona (+2.4%). In terms of RevPar, Athens recorded a decline, while the other three cities recorded positive changes.

As stated in the announcement by the Hellenic Chamber of Hotels, “the data reflect and confirm the feeling that most of us—people in the tourism industry as well as citizens—have about a ‘dangerous stagnation’ in the tourism performance of Athens and the country in general. We call on the State and Local Government to take into account the ‘messages’ from professionals in the sector and to focus in a timely manner on measures, strategies, decisions, actions, and goals that will strengthen the competitiveness of the tourism product, improve public infrastructure, upgrade the tourist experience and proposal for 2026, and strengthen our relationship with traditional markets as well as new ones, as there are already signs of interest in Athens with the new flights that have been announced.

We await with particular interest this year’s announcements by the Prime Minister at the Thessaloniki International Fair, hoping that there will be no repeat of the “unpleasant surprises” for the hotel industry similar to those of 2024 (see issues relating to an increase in the resilience fee, an increase in the tourist tax, etc.). On the contrary, we expect announcements that will give a boost, strengthen resilience and competitiveness, and contribute to the repositioning of Greek tourism—a sector that, as is well known, must innovate by constantly renewing its offering to international markets.

{kind=link}