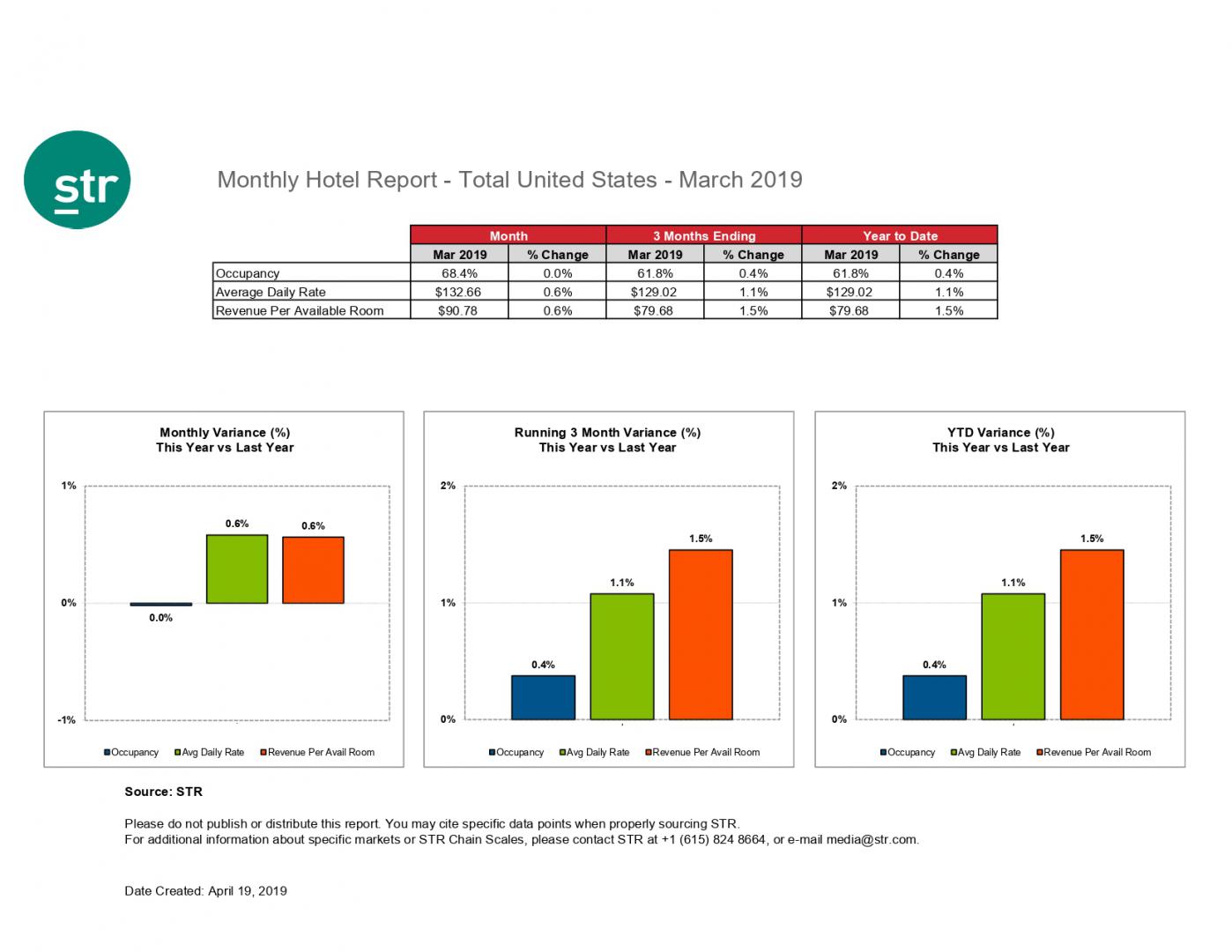

The U.S. hotel industry reported mostly flat results in the three key performance metrics during March 2019, according to data from STR.

In a year-over-year comparison with March 2018, the industry posted the following:

• Occupancy: flat at 68.4%

• Average daily rate (ADR): +0.6% to US$132.66

• Revenue per available room (RevPAR): +0.6% to US$90.78

“Considering there would have been a helpful pivot in group business because of the Easter calendar shift, this was probably the industry’s worst March since the recession,” said Jan Freitag, STR’s senior VP of lodging insights. “The 0.6% change in ADR was the lowest for any month in the U.S. since May 2010, which indicates that pricing confidence may have not yet reached its floor. On the plus side, we continue to break monthly demand records, which is keeping overall performance in the black. The challenge of course is maintaining profit margin during a time of rising labor costs.”

The industry has now posted year-over-year RevPAR growth for 108 of the past 109 months.

The longest overall expansion cycle in industry history lasted 112 months from December 1991 through March 2001.

Among the Top 25 Markets, San Francisco/San Mateo, California, posted the only double-digit increase in RevPAR (+10.0% to US$200.92), due to the only double-digit jump in ADR (+13.5% to US$251.51). Freitag noted that the market’s year-over-year performance continues to be helped by returned group business driven by the reopened Moscone Center. San Francisco results also continue to have a noticeable impact on overall U.S. results, lifting RevPAR by 0.2 percentage points in March.

Anaheim/Santa Ana, California, registered the largest increase in occupancy (+2.9% to 82.4%).

New Orleans, Louisiana, experienced the second-highest lift in RevPAR (+9.1% to US$155.19).

New York, New York, reported the only double-digit decline in RevPAR (-10.4% to US$184.25) because of the largest drop in ADR (-7.0% to US$218.98).

Philadelphia, Pennsylvania-New Jersey, saw the largest decrease in occupancy (-6.9% to 68.4%).

“On the whole, the top markets continue to underperform the rest of the country in year-over-year growth,” Freitag said. “New inventory entering those major cities is pulling occupancy levels down and further affecting hotelier pricing confidence.”

{kind=link}