The UBS Global Real Estate Bubble Index 2021, a yearly study by UBS Global Wealth Management’s Chief Investment Office, indicates that the bubble risk has on average increased during the last year, as has the potential of a severe price correction in many of the cities tracked by the index.

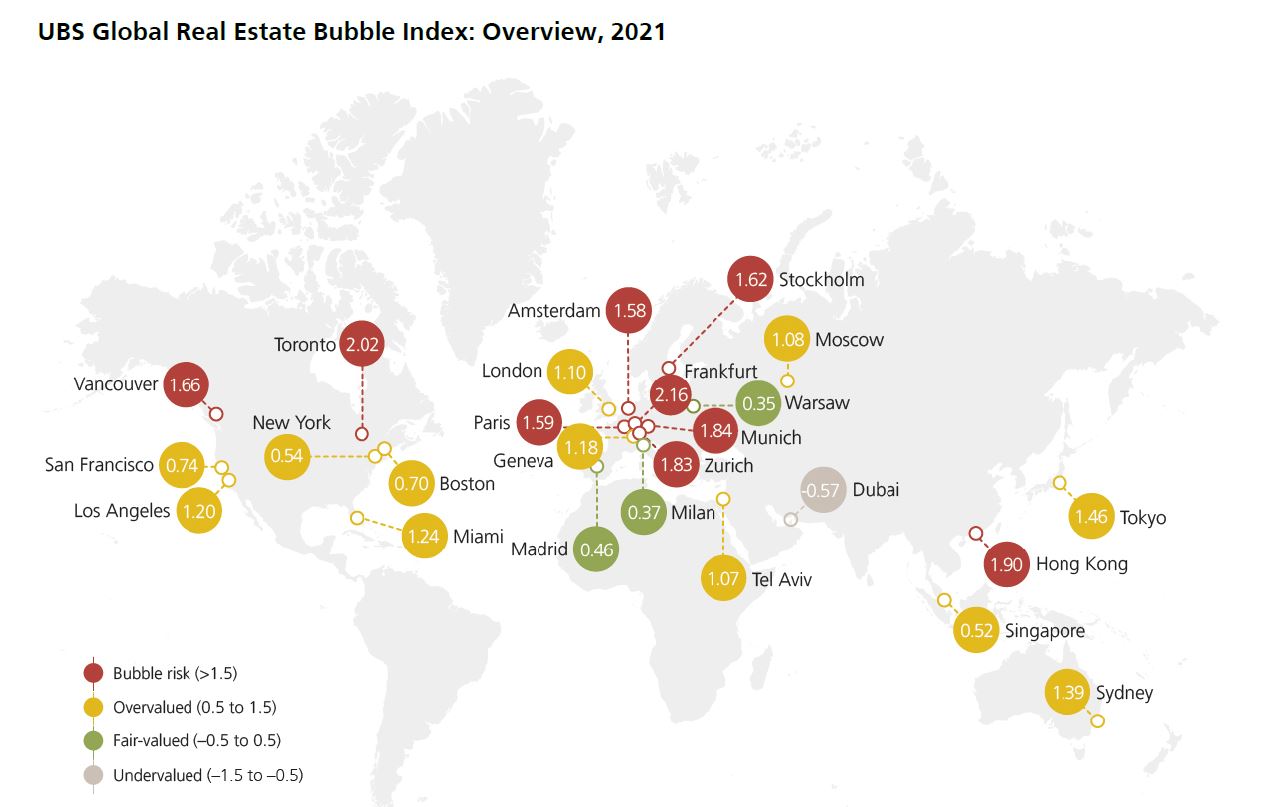

Frankfurt, Toronto, and Hong Kong top this year’s index, with the three cities warranting the most pronounced bubble risk assessments in the analyzed housing markets. Risk is also elevated in Munich and Zurich; Vancouver and Stockholm have both reentered the bubble risk zone. Amsterdam and Paris complete the list of cities with bubble risk. All US cities evaluated—Miami (replacing Chicago in the index this year), Los Angeles, San Francisco, Boston, and New York—are in overvalued territory.

Housing market imbalances are also high in Tokyo, Sydney, Geneva, London, Moscow, Tel Aviv, and Singapore, while Madrid, Milan, and Warsaw remain fairly valued. Dubai is the only undervalued market and the only one to be classified in a lower category than last year.

Housing market imbalances are also high in Tokyo, Sydney, Geneva, London, Moscow, Tel Aviv, and Singapore, while Madrid, Milan, and Warsaw remain fairly valued. Dubai is the only undervalued market and the only one to be classified in a lower category than last year.

Hot but likely short-lived housing boom

House price growth on average accelerated to 6% in inflation-adjusted terms from mid-2020 to mid-2021. All but four cities—Milan, Paris, New York, and San Francisco—saw their house prices increase. And double-digit growth was even recorded in five cities: Moscow; Stockholm; and the cities around the Pacific, Sydney, Tokyo, and Vancouver. A combination of special circumstances has sparked this price rally.

Claudio Saputelli, Head Real Estate at UBS Global Wealth Management’s Chief Investment Office, explained: “The coronavirus pandemic confined many people within their own four walls, amplifying the importance of living space, and leading to a higher willingness to pay for housing.” At the same time, already favorable financing conditions have improved even more as lending standards for home buyers have been relaxed. Moreover, higher saving rates and booming equity markets have freed up additional housing equity.

More leverage, more risk

The low user cost of owning property compared with renting at the moment, along with the expectation of ever-growing house prices, makes homeownership seemingly attractive for households, regardless of price levels and leverage. This rationale may keep markets running for the time being. But households have to borrow increasingly large amounts of money to keep up with higher property prices.

In fact, growth of outstanding mortgages has accelerated almost everywhere in the last quarters, and consequently debt-to-income ratios have risen. Overall, housing markets have become even more dependent on very low interest rates, so that tightening of lending standards could bring price appreciation to an abrupt halt in most markets. Nevertheless, leverage and debt growth rates are still well below their all-time highs in many countries. From this perspective, the housing market is unlikely to cause major disruptions on global financial markets for the time being.

In fact, growth of outstanding mortgages has accelerated almost everywhere in the last quarters, and consequently debt-to-income ratios have risen. Overall, housing markets have become even more dependent on very low interest rates, so that tightening of lending standards could bring price appreciation to an abrupt halt in most markets. Nevertheless, leverage and debt growth rates are still well below their all-time highs in many countries. From this perspective, the housing market is unlikely to cause major disruptions on global financial markets for the time being.

First-time urban housing underperformance in a quarter of a century

In addition to lower financing costs, urbanization was the main pillar of house price appreciation in city centers in the last decade. However, city life has suffered a considerable blow from lockdowns. Economic activity has spread outward from city centers to their (sometimes distant) suburbs and satellites—and so has the demand for housing. Consequently, for the first time since the early 1990s, housing prices in non-urban areas have increased faster than in cities over the last four quarters.

In addition to lower financing costs, urbanization was the main pillar of house price appreciation in city centers in the last decade. However, city life has suffered a considerable blow from lockdowns. Economic activity has spread outward from city centers to their (sometimes distant) suburbs and satellites—and so has the demand for housing. Consequently, for the first time since the early 1990s, housing prices in non-urban areas have increased faster than in cities over the last four quarters.

While some effects may be transitory, this reversal weakens the case for quasi-guaranteed house price appreciation in city centers. The impact of this shift in demand will likely be even bigger in regions with stagnating or even shrinking populations (e.g., in Europe), as supply will have an easier time keeping up with demand.

Matthias Holzhey, lead author of the study and Head Swiss Real Estate at UBS Global Wealth Management’s Chief Investment Office, concludes: “A long, lean spell for city housing markets looks more and more probable, even if interest rates remain low.”

Regional perspectives

Zurich’s housing remains in the bubble risk zone, and its score rose sharply between mid-2020 and mid-2021. The market has been overheating, and offered volumes have fallen to a record low. Especially in the bidding process, buyers are at risk of paying excessive prices relative to other Swiss regions, as expectations of rising prices are deeply entrenched. Furthermore, Zurich has the highest price-to-rent ratio among all analyzed cities, which makes the market very vulnerable to interest rate hikes. Zurich’s price and index scores also continue to top Geneva’s.

Zurich’s housing remains in the bubble risk zone, and its score rose sharply between mid-2020 and mid-2021. The market has been overheating, and offered volumes have fallen to a record low. Especially in the bidding process, buyers are at risk of paying excessive prices relative to other Swiss regions, as expectations of rising prices are deeply entrenched. Furthermore, Zurich has the highest price-to-rent ratio among all analyzed cities, which makes the market very vulnerable to interest rate hikes. Zurich’s price and index scores also continue to top Geneva’s.

Geneva’s index score has been on the rise since 2018 and is in overvalued territory. Prices have reached an all-time high, surpassing the previous peak in 2013. As Geneva’s rental market is highly regulated and rents are inflated, homeownership is still attractive, underpinned by historically low mortgage rates. In both Swiss cities, a broad market correction is not in the offing in the short run. Geneva continues to benefit from its relative stability and international status, and Zurich remains highly attractive as a business location and is enjoying robust employment growth. In the long run, however, there is cause for caution with regard to both cities. If interest rates trend higher and demand growth shifts away to the suburbs and periphery given low affordability in the city centers, today’s inflated prices may not be sustainable.

Europe

Imbalances remain sky-high in Frankfurt, Munich, Paris, and Amsterdam, cities from core Eurozone countries. Housing markets remain under the spell of the European Central Bank’s negative interest rate policy and easy lending standards. But price increases have slowed over the last year and fallen behind the respective national averages as city centers have become less affordable and demand has shifted to the suburbs and satellites. Nevertheless, a price correction is not imminent as long as job creation within these cities remains strong and interest rates stay negative. By contrast, the housing markets in Milan and Madrid were hit harder by the pandemic. Strict and long lockdowns brought housing market recoveries to a halt. A period of sustained and healthy economic growth would be needed to trigger a housing boom in these cities.

Although price growth in London still trails the nationwide average, the pandemic has led to the bottoming out of the city’s housing market, which remains overvalued. The rise of home and flexible office models sparked an increase in demand and accelerated price growth for homes with more space and greater affordability (i.e., outside of the city center). By contrast, Inner London’s housing market has been hit particularly hard by the pandemic. Benefitting from relaxed financing conditions, Moscow and Stockholm have recorded the highest price growth rates among all analyzed cities over the last four quarters, and the market imbalances have increased sharply. Warsaw’s housing market has remained fairly valued, as price growth has fallen behind the nationwide average.

Middle East

In Tel Aviv, falling mortgage rates and rapid population growth have pushed up prices. Moreover, the government has lowered the purchase tax for second homes, even encouraging housing market speculation as the market again approaches bubble risk territory. As a result, the market is highly overvalued. By contrast, prices in Dubai were still falling leading up to the end of 2020, and the market is now undervalued. Improved affordability, easier mortgage regulations, higher oil prices, and an economic rebound now seem to have finally kick-started a recovery. Although construction has slowed, essentially limitless supply poses a risk for long-term appreciation prospects.

APAC

Market imbalances increased in all analyzed APAC cities from mid-2020 to mid-2021. Hong Kong is the only market in the bubble risk zone, despite three years of nearly stagnating real estate prices. But the housing market shows signs of heating up again. Price growth has accelerated, and sales have even reached the highest level ever recorded, with robust housing demand in the upper price and luxury segment. That said, the government is eager to actively increase the new housing supply over the medium-to-long term, which could have structural price dampening effects. In Singapore house price and income growth were aligned for over two decades. Since 2018, however, stronger price growth has returned as the city has benefited from higher foreign demand. The market is in slightly overvalued territory, as prices have started to outpace rents and incomes. But imbalances still look moderate compared with most other cities analyzed in the study.

The correction period for Sydney’s housing market has been brief. Easier lending standards and the Reserve Bank of Australia´s rate cuts have reflated the market. Without a turnaround in interest rates, the decade-long upward trend of house prices is likely to continue given ongoing population growth. Real estate prices in Tokyo have been increasing almost continuously for over two decades, bolstered by attractive financing conditions and population growth. But the housing price level in the capital has decoupled increasingly from the rest of the country, leading to stretched affordability that will likely curb future price growth.

US

The index scores have been relatively stable over the last five years in the East Coast cities. By contrast, the West Coast markets have developed less consistently. In Los Angeles, the index score has continued to increase, while in San Francisco valuations have declined due to falling home prices. Overall, the drop of mortgage rates to historically low levels has supported house prices in the US. But price changes in the analyzed cities trail the nationwide average. Inner-city demand growth has slowed as citizens have moved out to the suburbs either because of affordability issues or in response to the impacts of COVID-19. Continued migration to lower-cost and more tax-, business-, and regulatory-friendly states has accelerated this trend.

About UBS

UBS provides financial advice and solutions to wealthy, institutional and corporate clients worldwide, as well as private clients in Switzerland. UBS is the largest truly global wealth manager, and a leading personal and corporate bank in Switzerland, with a large-scale and diversified global asset manager and a focused investment bank. The bank focuses on businesses that have a strong competitive position in their targeted markets, are capital efficient, and have an attractive long-term structural growth or profitability outlook.

UBS is present in all major financial centers worldwide. It has offices in more than 50 regions and locations, with about 30% of its employees working in the Americas, 30% in Switzerland, 19% in the rest of Europe, the Middle East and Africa and 21% in Asia Pacific. UBS Group AG employs more than 72,000 people around the world. Its shares are listed on the SIX Swiss Exchange and the New York Stock Exchange (NYSE).